An employee ownership trust (an EOT) is a form of employee trust offering indirect ownership of shares by employees. It is a collective vehicle which acquires a controlling interest in a company and then holds that interest for the long term benefit of the company’s employees.

Article / 7 Jan 2021

A practical guide to employee ownership trusts

Insight shared by:

-

What are the key benefits of an employee ownership trust?

EOTs were borne out of a desire to increase employee ownership of UK businesses. Studies have consistently shown that employee owned businesses perform better, demonstrating greater resilience, innovation and profitability. Employees show greater commitment to, and engagement with, a business when they have a stake in it.

To encourage a move to employee ownership, there are generous tax benefits available for owners who transfer their shares to an EOT. Significantly, such a sale can be made without attracting any charge to capital gains tax. With a standard rate of 20%, avoiding capital gains tax can provide a welcome boost to sale proceeds for those looking to exit a business.

-

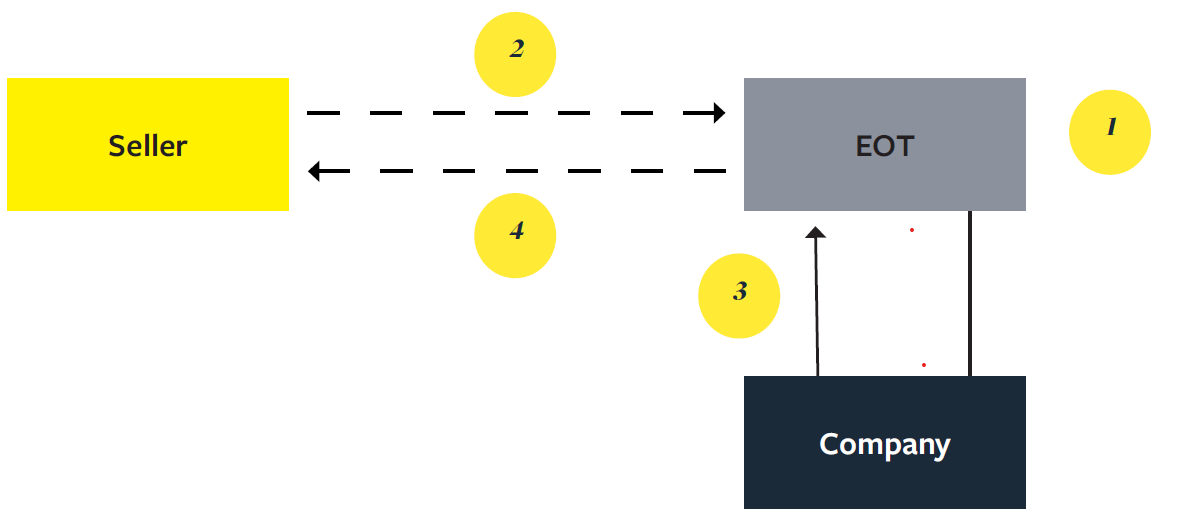

How is a sale to an employee ownership trust structured?

Step 1: The EOT is set up, governed by a detailed trust deed. Typically, the EOT will have a corporate trustee whose directors are usually a mix of executive directors of the target company, employee representatives elected by an Employee Council, possibly a seller and perhaps an independent professional trustee.

Step 2: The seller sells shares to the EOT with the EOT acquiring more than 50% of the shares. Although some consideration may be paid on completion, the majority will be left outstanding to be paid by the EOT on a deferred basis.

Step 3: The company funds the EOT from its ongoing profits.

Step 4: The EOT uses the funds it receives from the company to pay the deferred consideration to the seller over time, as the profits become available.

-

How is a sale funded?

The buyer of the shares is the EOT. But the EOT itself has no assets and no way of generating assets. So it will be reliant on other sources to pay for the shares.

In anticipation of the sale to the EOT the seller could allow profits to accumulate in the target company rather than, for example, extracting them by way of dividend. The company could then contribute those profits to the EOT for it to put towards paying the seller for the shares. But it’s unlikely the target company would be able to build up a reserve large enough to satisfy the entire consideration on completion.

It may be possible for the EOT to borrow money to help fund the purchase. But any lender would require security for that borrowing and, as noted above, the EOT has no assets which it can leverage as security. So a lender is likely to require a guarantee from the target company in respect of the borrowing by the EOT. This can give rise to problems for the directors of the target who are under a duty to act in the best interests of that company and it may also affect the ability of the target to borrow for its own business purposes in the future.

Alternatively, it may be possible for the target to borrow money from a bank and then pass that up to the EOT to fund the consideration. Again, however, this could give rise to directors’ duties issues – is borrowing to fund the EOT’s liability in the company’s best interests? Security will also be required which may not be possible, depending on what security the target has already granted, and again this could affect the target’s ability to borrow for its own purposes in the future.

Because of the above issues with borrowing to fund the consideration, it is usual for a large part (sometimes even all) of the consideration due to the seller to be paid in instalments as deferred consideration. As the target company generates profits, these are passed up to the EOT which it uses to pay the deferred consideration to the seller over a number of years.

-

What are the tax advantages?

- The key advantage for the seller is that there is no capital gains tax on a transfer of shares to an EOT. As long as the EOT acquires a controlling interest in the target company, all sellers that dispose of shares to the EOT in the same tax year qualify for this relief. This includes minority sellers who might not benefit from other available reliefs such as business asset disposal relief (previously known as entrepreneurs’ relief).

- The key advantage for the employees of the target company is that they can be paid tax free bonuses of up to £3,600 each per year. Although the bonuses are not subject to income tax, the company will still have to pay National Insurance contributions on them as HMRC view the relief as benefiting the employee not the employer.

- There is also relief from inheritance tax for certain transfers of shares into and out of the EOT.

-

What are the other advantages of an employee ownership trust?

Simply focusing on the tax benefits of selling to an EOT misses the broader advantages such a sale can bring. These include:

- Employee engagement: as noted above, greater employee engagement in the business will reap rewards for all those involved. Benefits include greater commitment, reduced absenteeism, a drive for innovation and increased profitability.

- Friendly-buyer: because a sale to an EOT is essentially an internal transaction, involving no third parties, it is generally viewed as being a “friendly” transaction, which is easier to negotiate. The sale process is often quicker and smoother when compared with a sale to a third party, and the seller can benefit from fewer residual liabilities under a reduced warranty and indemnity package.

- Ready-made exit: a sale to an EOT provides the seller with a ready-made exit from the business. This could be useful where the seller has struggled to find a buyer or where a family business is hampered by succession issues with the next generation being unable or unwilling to takeover. Entrepreneurs who have built up their business from scratch may prefer the idea of transferring ownership to employees rather than selling out to a competitor. It also avoids a founder having to work for a new owner at the end of their career which might happen on an exit to a private equity investor.

- Better return: as the sale proceeds are free from capital gains tax, the seller can receive a higher overall return when compared with a traditional sale. Alternatively, the increased return could allow the seller to offer the shares to the EOT at a discounted price without affecting the seller’s overall net proceeds.

- Retained shareholding: provided a “controlling interest” (see below) in the target company is transferred to the EOT, a seller can decide whether to sell all their shares or whether to retain a minority shareholding. By contrast, a trade seller would want to acquire 100% of the target company and any retained holding on a private equity deal would be subject to conditions. This could be useful for a seller who wants to hand over control of the business to its employees but who is not yet ready to fully withdraw from that the business.

- Management incentives: it is possible to combine the advantages for a seller of a sale to an EOT with the benefits for second-tier management of a traditional management buyout. Share incentive schemes, either through direct holdings in the target alongside the EOT or via tax efficient share option schemes, mean the next tier of management can receive some of the benefits of a buyout without the restrictions of an external investor protecting their investment.

-

What are the risks to the seller?

As noted above, it is usual for a large part of the consideration due to the seller on the sale of their shares to the EOT to be left outstanding, payable as deferred consideration. The seller will be reliant on the target company continuing to trade profitably after completion in order to generate the profits required to fund that consideration via the EOT. And whilst the consideration is payable over time, the sale price is fixed at completion. So if the value of the target increases after completion whilst the deferred consideration is outstanding, the seller won’t see an increase in their sale proceeds.

In order to satisfy the qualifying conditions, the seller must have no ongoing control over the target or the EOT. So the seller will be reliant both on the target’s directors resolving to use its profits to fund the consideration via the EOT, and on the trustees of the EOT resolving to apply the trust’s assets (ie the funds it receives from the target) to fund the deferred consideration.

The seller may be able to retain a seat on the target company’s board, or act as a trustee of the EOT. But this will only enable the seller’s voice to be heard – there can be no question of retaining any control.

-

What are the qualifying conditions which must be met?

In order to benefit from the associated tax reliefs there are a number of qualifying conditions which must be met:

- All employee benefit requirement: all eligible employees should benefit from the EOT. Those who hold or have previously held 5% or more of the target company’s shares are not eligible employees. It is also possible to exclude employees with less than 12 months’ continuous service.

- Equality requirement: all eligible employees must benefit from the EOT on the same terms. This does not mean that all employees get equal amounts and it is possible to determine the size of awards by reference to remuneration, length of service and hours worked.

- Controlling interest requirement: the EOT must acquire and retain a “controlling interest” in the target company. A “controlling interest” means more than 50% of the ordinary share capital, more than 50% of the voting rights and an entitlement to more than 50% of the profits available for distribution by the company.

- Limited participator requirement: broadly the number of people who are 5% shareholders and officers or employees of the company cannot exceed 2/5ths (40%) of the total number of employees of the company. This could be an issue for a company with a small workforce compared to the number of 5% shareholders who are officers or employees.

- Trading requirement: the target company whose shares are being acquired by the EOT must be a trading company or the holding company of a trading company.

-

What happens if there is a disqualifying event?

Breaching the qualifying conditions can have consequences for both the seller and the EOT. A breach could occur in various ways, for example:

- the EOT could sell some or all of its shares in the target company meaning the controlling interest requirement is no longer satisfied;

- the EOT could permit awards to employees on unequal terms meaning the equality requirement is no longer met; or

- the number of participators in the company could exceed 40% of the workforce breaching the limited participator requirement.

If a disqualifying event occurs in the first tax year following the disposal to the EOT, the capital gains tax relief can be clawed back from the seller.

If a disqualifying event occurs in or after the second tax year following the disposal to the EOT, there is a deemed disposal and immediate re-acquisition at market value by the EOT of all the shares it holds in the target company. This would result in a tax charge for the EOT. And satisfying that tax charge would reduce the assets in the EOT available to pay the deferred consideration to the seller.

Whether or not a disqualifying event occurs is generally within the control of the EOT trustee. So the seller will be reliant on the trustee not taking any deliberate action, such as a sale to a third party, which could be a disqualifying event.

Get in touch

The significant advantages of a sale to an EOT could provide a welcome solution for anyone looking to exit a business as well as those who want to transfer ownership to the workforce for purely altruistic reasons. Such a sale is not without risk for a seller, but that risk comes in return for the generous tax relief available. Making sure that the sale is properly structured and documented is key to minimising these risks and ensuring that all parties involved secure the best possible outcome.

For further guidance please contact an expert listed below or visit our employee ownership trusts service page for more information on how we can help you.